Whether you are considering the

purchase of your first home or trading up to the home your family frequently

fantasizes about, there are three crucial questions you must know the answer

to:

1.

What

is the minimum down payment required to purchase a home?

2.

What

is the minimum FICO score required to qualify

for a mortgage?

3.

What

is the maximum Back-End DTI Ratio allowed?

A

survey conducted by Fannie Mae revealed startling information: most

Americans don't know the answer to these three crucially important questions.

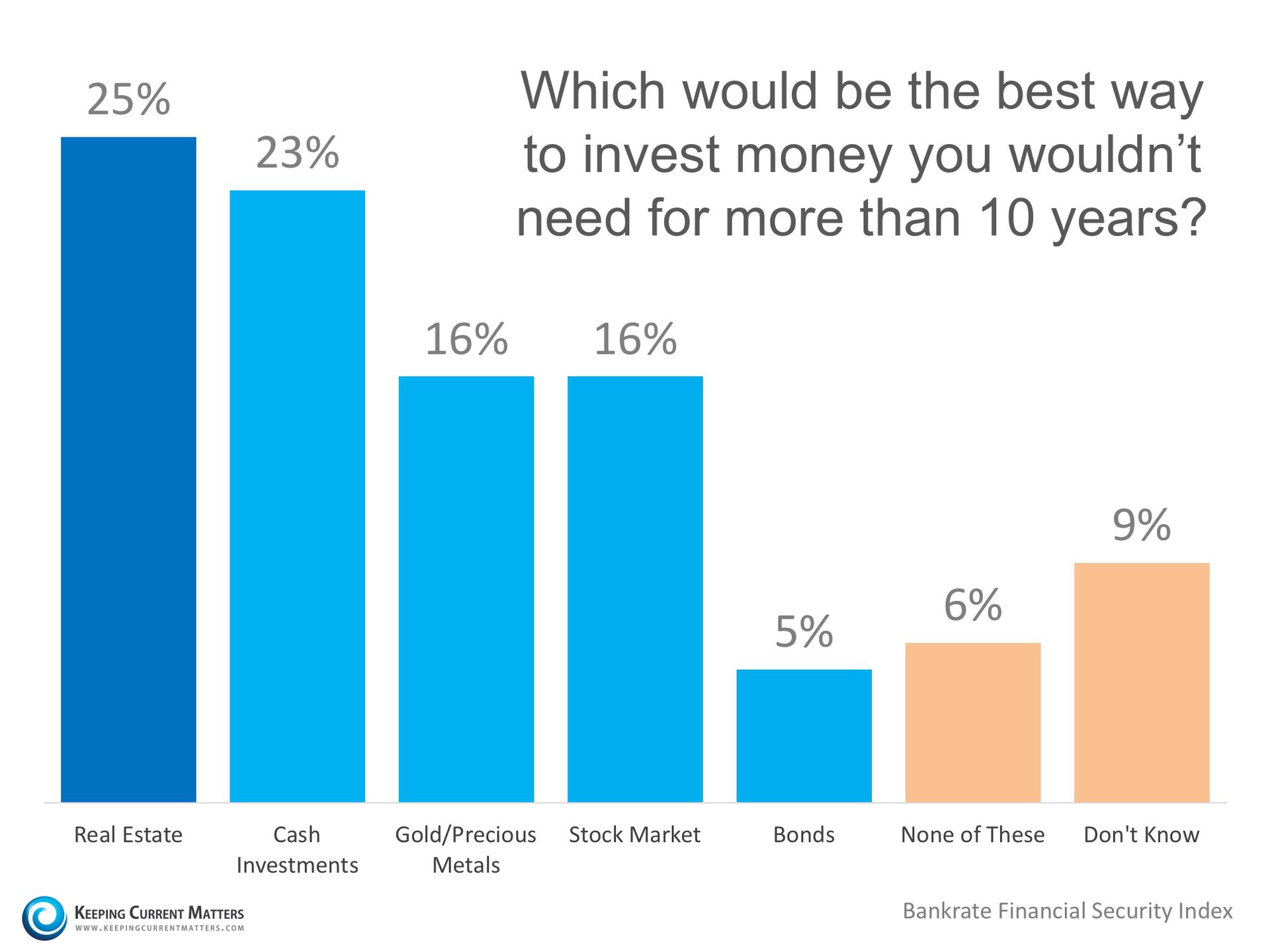

Here is a graphic showing the results of the survey:

The percentages are quite

disturbing but can explain why so many people believe they are not

eligible to purchase a home whether it is a first home or a trade-up

home. Here are the actually requirements as

per Fannie Mae:

Bottom Line

If you are considering purchasing a home, make sure you are aware of all your options before moving forward.

If you are considering purchasing a home, make sure you are aware of all your options before moving forward.

David Demangos

858.232.8410

Locally Known, Globally Connected

Luxury Home Marketing Specialist

Global Property Specialist

David@AwesomeSanDiegoRealEstate.com

Our Team Goes to Extremes to Fulfill Your Real Estate Dreams!