You may be wondering if home prices are going to crash. And believe it or not, some people might even be hoping this happens so they can finally purchase a more affordable home. But experts agree that's not what's in the cards – and here's why.

There are more people who want to buy a home than there are homes available to purchase. That’s what drives prices up.

Let’s break that down and explore why, nationally, home prices aren’t going to be coming down anytime soon.

Prices Depend on Supply and Demand

The housing market works like any other market – when demand is high and supply is low, prices rise.

According to the latest estimates, the U.S. is facing a housing shortfall of several million homes. That means there are far more people looking to buy (demand) than there are homes for sale (supply). That mismatch is the key reason why prices won’t fall at the national level. As David Childers, President of Keeping Current Matters (KCM), puts it:

“The main driving force on pricing is the limited amount of inventory in most markets across the country. That issue is not going to be solved overnight or in the next twelve months.”

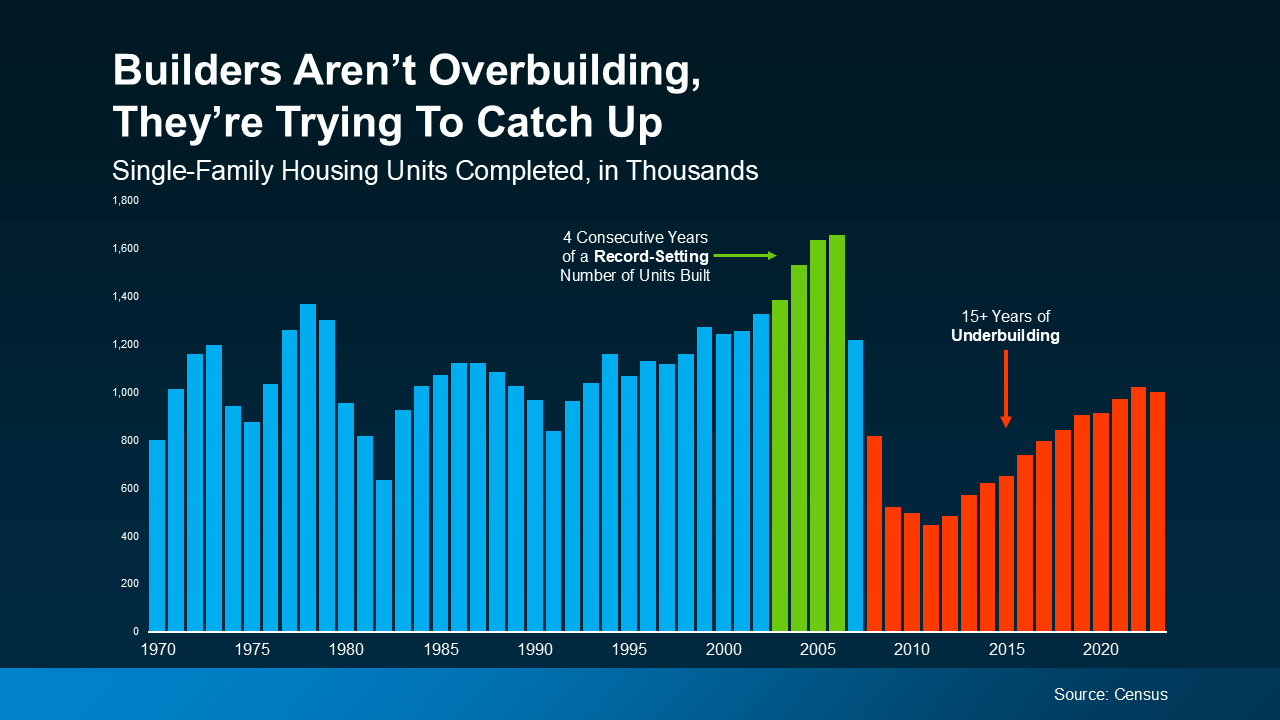

How Did We Get Here?

For over 15 years, homebuilders haven’t been building enough homes to keep up with buyer demand. After the 2008 housing crisis, homebuilding slowed significantly, and it’s only recently started to recover (see graph below):

Even with new construction on the rise over the past few years, builders are playing catch-up. And according to AmericanProgress.org, they’re still not even keeping up with today’s demand, let alone making up for years of underbuilding.

Even with new construction on the rise over the past few years, builders are playing catch-up. And according to AmericanProgress.org, they’re still not even keeping up with today’s demand, let alone making up for years of underbuilding.

And as long as there’s a housing shortage, home prices will remain steady or increase in most areas.

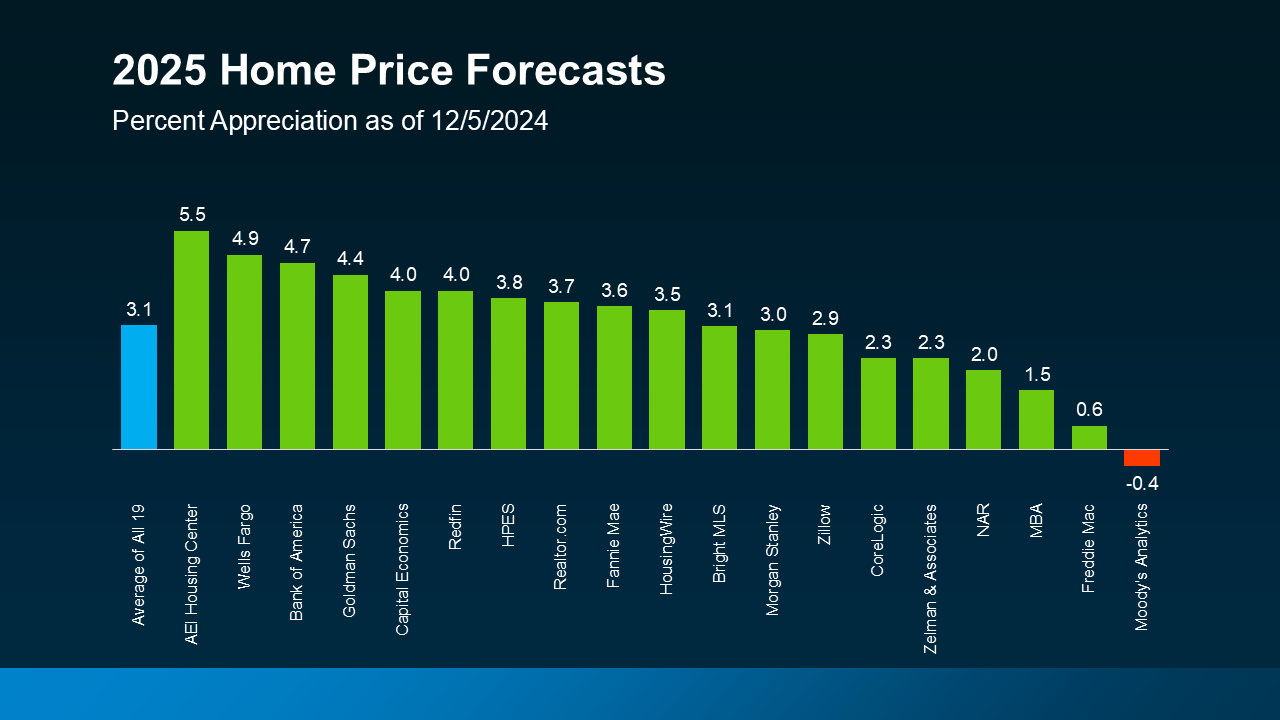

What About Next Year?

The majority of experts agree prices will keep rising next year, but at a much slower, healthier pace (see graph below):

But it’s important to note home prices vary by market. What happens nationally might not reflect exactly what’s happening in your area. If your local market has more inventory available, prices could grow more slowly or even decline slightly. But in areas where inventory remains tight, prices will keep climbing – and that’s what’s happening throughout most of the country. That’s why it’s crucial to work with a local real estate expert who understands your market and can explain what’s going on where you live.

But it’s important to note home prices vary by market. What happens nationally might not reflect exactly what’s happening in your area. If your local market has more inventory available, prices could grow more slowly or even decline slightly. But in areas where inventory remains tight, prices will keep climbing – and that’s what’s happening throughout most of the country. That’s why it’s crucial to work with a local real estate expert who understands your market and can explain what’s going on where you live.

If you’re wondering what it’ll take for prices to come down, it all goes back to supply and demand. With inventory still limited in most markets, prices are likely to remain steady or rise.

To see what’s happening with home prices where we live, let’s connect. That way you’ll have help understanding our market and making a plan that works for you.